Actuarially Speaking

Hawaii pension fund relies on highly educated guesses of what the future holds.

By no measure is it a best-seller, but for the staff of the Hawaii Employees’ Retirement System the annual actuarial valuation is a must read.

With more than 100 pages of numbers, percentages and projections, the report sketches a picture of what it will take to guarantee the financial security of nearly 116,000 current and retired public employees and their dependents.

Produced by experts using calculators, not crystal balls, this yearly peek into the future sets the tone for decisions involving billions of dollars in public money and impacts every government budget in Hawaii.

Actuarial valuations are to pension funds what navigation systems are to airliners, giving pension administrators and trustees an idea of where they should be going and how long it will take to get there.

Actuaries are highly skilled professional statisticians who compile and analyze economic, demographic and other data, utilizing mathematical formulas to calculate the probability of future occurrences and estimating the financial impact. In its most basic form, the actuarial study is a complex numbers game resulting in conclusions ranging from the mundane, such as how many public employees will take early retirement, to the macabre – when will retirees die and how much will their pensions cost before they do.

The primary actuarial concept applying to pension funds is that of “present discounted value” — the idea that $1 today will be worth more than $1 in the future because today’s dollars can be invested and earn interest. These are calculations that predict the value of pension payments decades into the future and the value of those obligations in today’s dollars.

These assumptions — such as the expected rate of return on investments, life expectancies of retirees, inflation and other factors — are, literally, highly educated guesses about whether there will be future market crashes, recessions or other unforeseen economic events adversely impacting ERS assets and revenues.

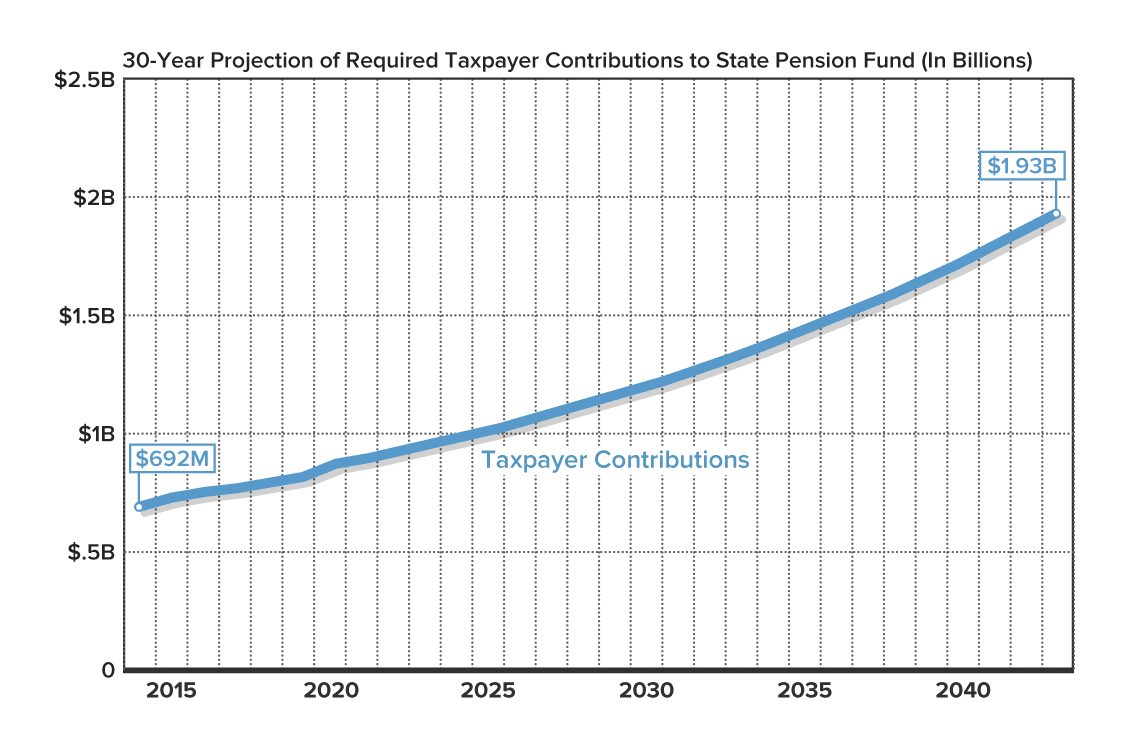

This is a critical factor for state and local government because it is the basis for establishing the Annual Required Contribution — the amount that must be budgeted and paid each year to ensure there will be enough money for pension payments a half-century from now. It also guides ERS investment strategy.

Annual contributions established by the actuarial evaluations can be substantial. For example, last year the state paid $418.4 million toward pensions, about 8 percent of its general fund revenue. The City and County of Honolulu paid $87.8 million, almost 9 percent of what its general fund collected in taxes and other income.

These payments might have been greater except for an accounting gimmick used by virtually every public pension fund – a practice called “smoothing,” designed to eliminate fluctuations in asset values and investment returns created by swings in financial markets. This is accomplished by spreading out, or smoothing, gains and losses over a predetermined period of time – four years in the case of the ERS – and is the basis for establishing the actuarial value of the assets.

Since a portion of the annual contributions by state and local government are designed to pay off the unfunded ERS liability – currently almost $8.5 billion — the greater the value of its assets the lower the unfunded liability will be and the less government will have to contribute, reducing pressure on annual budgets.

Some critics of smoothing say the practice is deceptive, making it difficult to determine the true financial status of a pension fund at any given point, and a more accurate measure would be to value assets at their market price – the price at which those assets could be sold at any particular moment.

For example, on June 30, 2013 the actuarial, or smoothed, value of ERS assets was $12.74 billion while the market value was $12.35 billion. During the height of the financial meltdown smoothing made ERS numbers look better. On June 30, 2009 the ERS reported the actuarial value of its assets at $11.4 billion, while the market value was $8.8 billion.

Because nearly two-thirds of ERS assets are invested in the stock market, large fluctuations in stock prices have major impacts on asset values and investment income. During the financial crisis, the market value of ERS assets dropped almost $2.6 billion and it suffered almost $2.9 billion in lost investment income.

However, as a long-term investor the ERS can afford to ride out the bad times and with the stock market soaring, the ERS has been able to make up much of its losses. On Dec. 31 the ERS reported assets of $13.5 billion. In just 18 months the market value of ERS stock has jumped 41 percent to $8.5 billion.

Wes Machida, the ERS executive director, said he pays more attention to market value because if the pension fund was forced to sell everything today that’s the amount of money he’d have to pay out.

Smoothing “has its benefits,” he said, “but as for me, I look at it from the standpoint of what’s available now and not necessarily what may be available or is spread out over the next four years.”